Your Money, Your Rules: Debt Funds for Financial Security

When you think about your finances, which aspect makes you feel secure? For many investors, it is the confidence that their investment portfolio is well-diversified and risk-adjusted. To achieve this sense of security, you need a well-balanced investment portfolio, in which each component, particularly debt funds, holds significant value.

Relatively low returns and hedge against volatility

Debt funds invest in instruments such as corporate bonds, treasury bills, commercial paper, and certificates of deposit. Unlike stocks, the values of these instruments do not fluctuate as easily. Thus, debt investments potentially add a layer of stability to your portfolio mix.

While it is true that equities can provide higher returns, they may not suit every investor's risk appetite owing to their inherent volatility, which is directly tied to the stock market's performance. Debt funds cater to investors who seek more predictable financial outcomes and low risk levels. The potential financial growth from debt funds may not be as high as those of equity funds, but this growth does not diminish rapidly with changing market conditions, which reduces the overall risk. Debt fund can be good for short-term goals and emergency funds

Different types of debt funds can be used to fulfil short-term goals and emergency fund needs. For example:

- Overnight funds invest in securities with one-day maturities. They offer a safe avenue for your capital to potentially experience financial growth with immediate liquidity.

- Liquid funds invest in high-quality debt instruments with a maximum maturity period of 91 days.

- Ultra-short duration funds invest in debt securities and money-market instruments. The Macaulay duration of the portfolio is 3–6 months.

- Low-duration funds have portfolio durations of 6–12 months.

- Short-term debt funds invest in instruments with slightly longer maturities. The investment horizons or maturity periods of these funds range between 1 and 3 years.

These funds are ideal for keeping surplus funds aside for upcoming expenses such as a holiday or a big-ticket purchase. In fact, liquid funds can be used to park emergency funds for medical expenses, home repairs, or unplanned travel needs. This flexibility makes them a prudent choice for cautious investors, as well as those with a more spontaneous approach to financial planning.

Liquidity

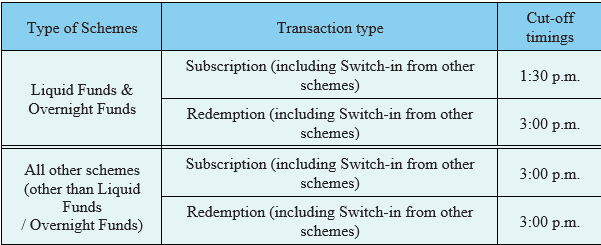

Many debt fund investments tend to offer high liquidity, which is a major benefit for investors. Once you place a redemption request before the cut-off time, the amount usually reflects in your bank account on the next working day. Refer the below table:

This feature is extremely useful for investors with urgent fund requirements.

Moreover, certain debt funds, such as liquid funds and overnight funds, offer an instant redemption facility. You can withdraw up to 90% of your unit value or ₹50,000 (whichever is lower)i. This facility gives offers the advantage of same-day withdrawal and same-day credit to your bank account. You can address personal financial needs quickly without the usual delays associated with many other types of investments.

Low cost structure

A high expense ratio can impact the potential financial growth of your scheme because mutual funds deduct these fees from your investments. However, debt funds offer a more affordable cost structureii.

As per the norms of the Securities and Exchange Board of India (SEBI), the Total Expense Ratio (TER) of a debt fund cannot exceed 2% of its Assets Under Management (AUM)iii. This ratio covers all costs of managing and running the fund, including management fees, administrative expenses, and other operating charges. A lower TER means that more of your capital is allocated instead of being used to cover expenses.

Multiple options to invest

You can invest in debt funds in different ways. You can make a lump sum investment in a debt scheme for a prompt and substantial participation in the market. Alternatively, small, regular investments can be made through systematic investment plans (SIPs) if you prefer to make consistent and manageable contributions.

You can also move units between different funds by using systematic transfer plans (STPs). The frequency can be weekly, monthly, quarterly, or half-yearly. This lets you decide how to use and allocate your capital, helping you tweak your investment plan to your preferences.

Aim to Risk-proof your portfolio with the help of debt funds

As you can see, debt funds can play an important role in any investment strategy. Their features such as relatively low risk, stability, income, and diversification make them prudent for both short- and long-term goals. Notably, debt funds are affected by inflation, credit, and interest rate risks, but these risks can be minimized through strategic management.

Source: Axismf Research

i: https://www.amfiindia.com/investor-corner/knowledge-center/cut-off-timings.html

ii: https://www.amfiindia.com/investor-corner/knowledge-center/Expense-Ratio.html

iii: https://www.amfiindia.com/investor-corner/knowledge-center/Expense-Ratio.html

Note: Views and opinions contained herein are for information purposes only and should not be construed as investment advice/ recommendation to any party or solicitation to buy, sale or hold any security or to adopt any investment strategy. It does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. The recipient should exercise due caution and/ or seek professional advice before making any decision or entering into any financial obligation based on information, statement or opinion which is expressed herein. No representation or warranty is made as to the accuracy, completeness or fairness of the information and opinions contained herein. The AMC reserves the right to make modifications and alterations to this statement as may be required from time to time.

Statutory Details: Axis Mutual Fund has been established as a Trust under the Indian Trusts Act, 1882, sponsored by Axis Bank Ltd. (liability restricted to Rs. 1 Lakh). Trustee: Axis Mutual Fund Trustee Ltd. Investment Manager: Axis Asset Management Co. Ltd. (the AMC). Risk Factors: Axis Bank Limited is not liable or responsible for any loss or shortfall resulting from the operation of the scheme.

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All