10 Key Reasons to Invest in Axis Nifty India Defence Index Fund

India's defence sector has been getting a lot of attention lately. Here is a clear look at what is driving that interest and why it may be worth your attention as a long-term investor.

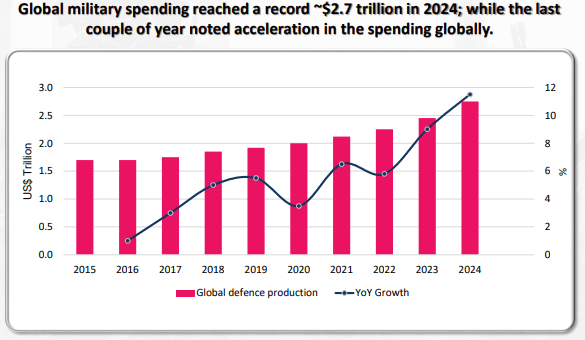

1. Global military spending hit $2.7 trillion in 2024 and it is still climbing:

Global defence spending reached $2.7 trillion in 2024, with year-on-year growth accelerating since 2021.

Every major region is increasing its military budget as shown by the following examples:

Europe: $563 billion in 2025, growing at 12.6% year-on-year. NATO has committed to spending 5% of GDP on defence by 2035, which anchors procurement plans well beyond this decade.

Asia: $573 billion in 2025. China alone accounts for 44% of Asia's total defence spending.

Middle East & North Africa: $219 billion in 2025, sustained by active conflicts across the region.

Defence procurement cycles run over years and sometimes decades. Spending commitments made today translate into orders that get executed well into the future.

2. Governments moving towards domestic manufacturers and modernisation:

Across the world, armed forces are upgrading to technology-intensive systems. These include surveillance infrastructure, precision-guided munitions, electronic warfare capabilities, and drone platforms. They require ongoing maintenance contracts, software upgrades, and component replacements over multi-year cycles. An initial government order is often the beginning of a revenue relationship that runs for a decade or more. . Alongside this, governments are redirecting procurement budgets toward domestic manufacturers. Countries that rely on imported defence equipment face a supply-chain risk in any conflict scenario. Building domestic capability is therefore a security priority and the policy direction in most major economies reflects that. Companies inside these domestic supply chains are seeing more orders, supported by steady demand from policy.

3. Active border tensions across multiple regions are keeping defence budgets from coming down

The Russia-Ukraine war, ongoing friction in the Middle east, and instability across West Asia have pushed governments into sustained procurement programmes. Countries that have committed to large military build-ups over the past two years are now working through multi-year execution plans. These spending commitments are already approved, contracts are being signed, and production timelines are set. Even if diplomatic conditions improve in any one region, the procurement cycles currently underway will continue running.

4. World order is moving from Unipolar to a Multipolar model:

For roughly three decades after 1991, global military spending as a share of GDP declined steadily. Countries with access to the US-led security umbrella had less pressure to invest heavily in their own forces. Rising tariffs, supply-chain disruptions, and the growing assertiveness of multiple large economies have made governments reconsider how much they can depend on external security arrangements.In a world with multiple competing powers, every country that wants strategic independence needs its own military capability. India, China, Brazil, Russia, and the European nations are all investing in this direction, resulting in a broad-based durable increase in global defence spending that plays out over years.

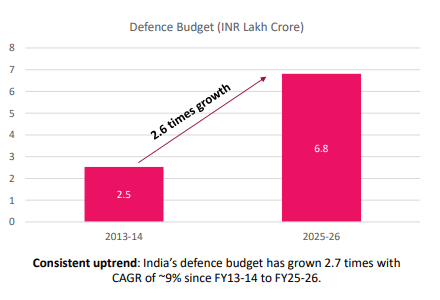

5. India's defence budget has grown 2.7 times since FY14: India's defence budget grew from ₹2.53 lakh crore in FY14 to ₹6.81 lakh crore in FY26, a CAGR of roughly 9%.  The Ministry of Defence now accounts for the highest allocation of 15% of total Union Budget expenditure.

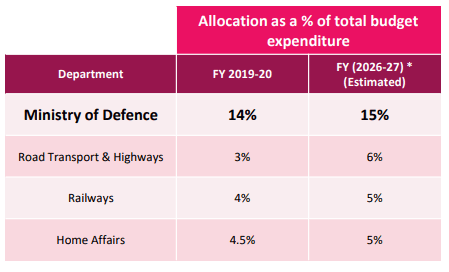

The Ministry of Defence now accounts for the highest allocation of 15% of total Union Budget expenditure.  The capital outlay portion of the defence budget, the part that directly funds procurement and manufacturing contracts, accounts for 23.6% of the total. With active security concerns on India's northern and western borders, this level of allocation has strong political consensus behind it too.

The capital outlay portion of the defence budget, the part that directly funds procurement and manufacturing contracts, accounts for 23.6% of the total. With active security concerns on India's northern and western borders, this level of allocation has strong political consensus behind it too.

6. India’s defence manufacturing push and policy backing:

Three policy decisions have reshaped India's defence procurement budget :

100% private participation: Allowed in defence manufacturing.

FDI permitted up to 74% in the sector.

Positive indigenisation lists which ensures that the procurement budget also flows to our Indian companies.

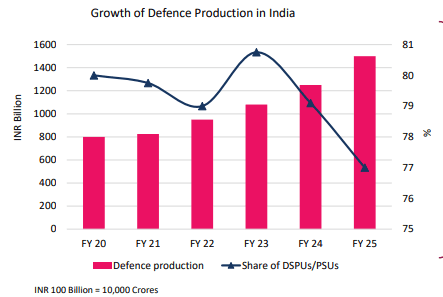

India's defence production has grown from ₹80,000 crores in FY20 to ₹1,50,000 crores in FY25. The government's target is ₹3,00,000 crores in annual production by 2029. . Defence PSUs currently account for about 77% of output, with private companies steadily expanding their share. For companies in this supply chain, domestic policy is creating predictable, long-duration demand.

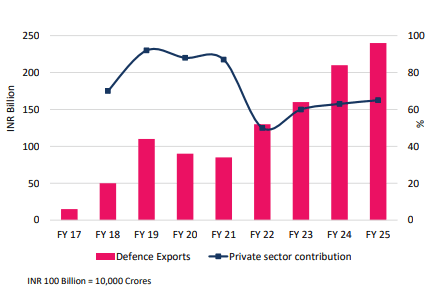

7. India's defence exports have grown more than 10x in 8 years:

India's defence exports in FY17: ₹2,000 crore

India's defence exports in FY25: ₹23,622 crore

Government export target by 2029: ₹50,000 crore

Countries India export equipment to: 85+ including the US, France, and Armenia. I

The product range now includes complete platforms: The BrahMos cruise missile, the Akash air defence system, the Pinaka rocket system, Advanced Light Helicopters, Dornier aircraft, and naval vessels.Export revenue gives Indian defence companies a second source of growth alongside domestic procurement while reducing dependence on any single government budget cycle.

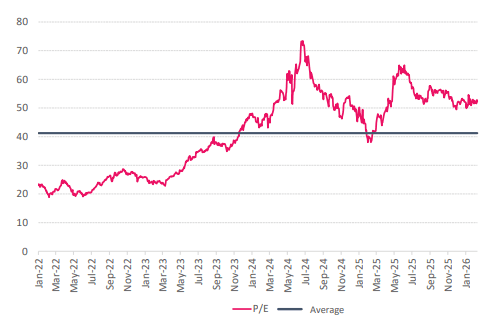

8. Valuations have come down significantly from their 2024 peak:

A P/E ratio tells you how much investors are paying for every rupee a company earns. A higher P/E means investors are paying a premium, expecting strong future growth.At their peak in mid-2024, the Nifty India Defence Index was trading at a P/E of over 70x which is relatively expensive. By early 2026, that has come down to the low 50x, trending toward the long-term average of 40x.

Defence companies tend to carry higher P/E ratios because their order books are long and revenue is contracted years in advance. The companies in this index also operate in specialised segments with limited direct competition. Earnings growth from government ordering, exports, and production scale-up could further bring this multiple down. Policy changes and procurement delays remain genuine risks and may affect valuations quickly.

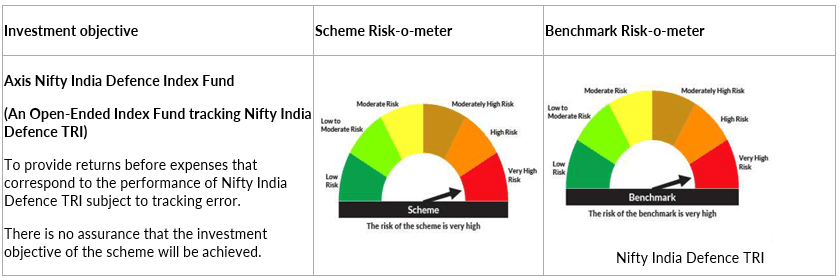

9. Axis Nifty India Defence Index Fund: Exposure across the entire defence value chain:

Axis Nifty India Defence Index Fund tracks the Nifty India Defence Index, which comprises companies from Aerospace & Defence, Explosives, and Shipbuilding industries or are Society of Indian Defence Manufacturers (SIDM) members with at least 10% of revenues from defence.

Top holdings (as of March 31, 2026): Bharat Electronics, Hindustan Aeronautics, Bharat Forge, Solar Industries, Mazagaon Dock, Cochin Shipyard, Bharat Dynamics.

Sector split: Aerospace & Defence, Auto Components, Explosives, Shipbuilding.

Weight cap: 20% per stock, to limit concentration at the top.

As a passive index fund, its benefits are as follows:

Rules-based selection: Eliminates human bias in selection

Seamless access to the defence sector: Covers the entire defence supply chain without having to research and screen individual stocks

Reconstituted every six months: Portfolio stays aligned with the sector automatically

Lower cost structure: Passive funds typically have lower costs than active funds

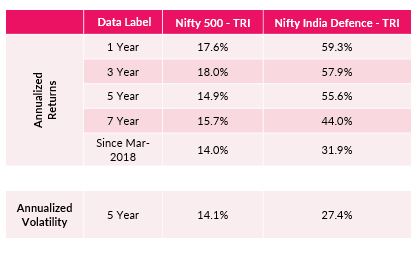

10. Historical performance:

Nifty India Defence TRI has delivered annualised returns above the broader market across every time period below:

It should be noted that the 5 year annualised volatility of 27.4%* is roughly double* that of the Nifty 500, suggesting higher volatility. As defence spending is driven by government procurement decisions, any change in budget priorities, procurement delays or export policy changes can affect the sector quickly.

Therefore, this fund may be suitable for investors with a long-time horizon and a very high risk appetite.

Investors should consult their financial advisors if in doubt about whether the product is suitable for them. The product labelling assigned during the New Fund Offer is based on internal assessment of the Scheme Characteristics or model portfolio and the same may vary post NFO when actual investments are made.

Sources:

https://www.sipri.org/sites/default/files/2025-04/2504_fs_milex_2024.pdfhttps://www.govconexec.com/2026/02/global-defense-spending-2025/https://www.sipri.org/sites/default/files/2025-04/2504_fs_milex_2024.pdfhttps://www.iiss.org/online-analysis/military-balance/2026/02/global-defence-spending-continues-to-grow-amid-geopolitical-uncertainty/.https://data.worldbank.org/indicator/MS.MIL.XPND.GD.ZS?end=2024&start=1960&view=charthttps://www.pib.gov.in/PressReleasePage.aspx?PRID=2191937®=3&lang=2).https://www.indiabudget.gov.in/https://www.indiabudget.gov.in/(https://www.pib.gov.in/PressReleasePage.aspx?PRID=2191937®=3&lang=2)(https://www.pib.gov.in/PressReleasePage.aspx?PRID=2154551&utm)(https://www.pib.gov.in/PressReleasePage.aspx?PRID=2154551®=3&lang=2).(https://indexpe.in/nifty-india-defence?utm).

Statutory Details: Axis Bank Limited is not liable or responsible for any loss or shortfall resulting from the operation of the scheme.

This article represents the views of Axis Asset Management Co. Ltd. and must not be taken as the basis for an investment decision. Neither Axis Mutual Fund, Axis Mutual Fund Trustee Limited nor Axis Asset Management Company Limited, its Directors or associates shall be liable for any damages including lost revenue or lost profits that may arise from the use of the information contained herein. No representation or warranty is made as to the accuracy, completeness or fairness of the information and opinions contained herein. The AMC reserves the right to make modifications and alterations to this statement as may be required from time to time. The article is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Opinions, if any, expressed are our opinions as of the date of appearing on this material only. While we endeavor to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Recipient shall understand that the aforementioned statements cannot disclose all the risks and characteristics. The recipient is requested to take into consideration all the risk factors including their financial condition, suitability to risk return, etc. and take professional advice before investing. The sector mentioned herein are for general assessment purpose only and not a complete disclosure of every material fact. It should not be construed as investment advice to any party. The schemes may or may not have any investments in stocks under these sectors.

NSE Disclaimer: It is to be distinctly understood that the permission given by NSE should not in any way be deemed or construed that the SIDs / Schemes of Axis MF has been cleared or approved by NSE nor does it certify the correctness or completeness of any of the contents of the SIDs. The investors are advised to refer to the SIDs for the full text of the 'Disclaimer Clause of NSE. The fund manager(s) may or may not choose to hold the stock mentioned, from time to time. Investors are requested to consult their financial, tax and other advisors before taking any investment decision(s).

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All