5 Steps to Invest in ELSS Funds

As written on 16th Feb 2021

Mutual fund schemes like equity schemes are known to offer capital appreciation over the long term. However, before investing in any type of mutual fund scheme, there are few things that an investor needs to take into consideration. For example: What are your goals? Which scheme is more suitable for your investment objective? Which scheme’s investment objective aligns with that of yours? What is the expense ratio of the fund?

Mutual funds are a pool of professionally managed funds that offer active risk management. However, because schemes such as equity mutual funds are a high risk investment, investors should first understand their risk appetite and discuss their financial goals with a financial advisor before taking an investment decision. The same applies to those seeking investment in tax saving schemes like ELSS. Equity Linked Savings Scheme (ELSS) is a tax saving mutual fund scheme that comes with a statutory lock in period of 3 years* and tax benefit. ELSS predominantly invests in equity markets which means that returns from ELSS are subject to market performance. The three year lock-in period means investors cannot redeem their ELSS fund units for at least three years from the date of purchase. Having said that, one should understand that among tax saving schemes that fall under Section 80C, ELSS has the lowest lock-in period .

Here’s an example to help you understand how ELSS helps with saving tax :

Ms. S, a senior marketing professional earns Rs. 12.5 lakh per annum. This lands her in the highest tax slab. Ms. S learns about ELSS through a colleague and decides to invest Rs. 1.5 lakh in it. According to the Section 80C of the Indian Income Tax Act, 1961, investments of up to Rs. 1.5 lakh made in an ELSS scheme are eligible for tax benefits. So, by investing Rs. 1.5 lakh in ELSS, S managed to bring down her gross taxable income to Rs. 11 lakh. Also, since ELSS is an equity mutual fund scheme, the 3 year lock in period might help S accrue some interest on the investment amount.

If you too want to save tax this fiscal year by investing in an ELSS fund, follow these five simple steps to make your investment journey simpler:

Understand your risk appetite

ELSS is an equity oriented scheme that is highly volatile in nature. One can even face losses over the short term. Hence, investors are expected to first determine their risk appetite before investing in this tax saving scheme.

Determine how much you need to invest in ELSS scheme

Talk to your financial advisor and tell them that you want to invest in an ELSS fund for saving taxes. After analyzing and breaking down your gross annual salary, the financial advisor might help you understand which tax bracket you currently fall under and accordingly suggest how much you need to invest in order to save tax. It is essential to understand the exact taxable income before investing, and hence, we suggest you take the help of your financial advisor for this crucial step.

Decide which ELSS fund you want to invest in

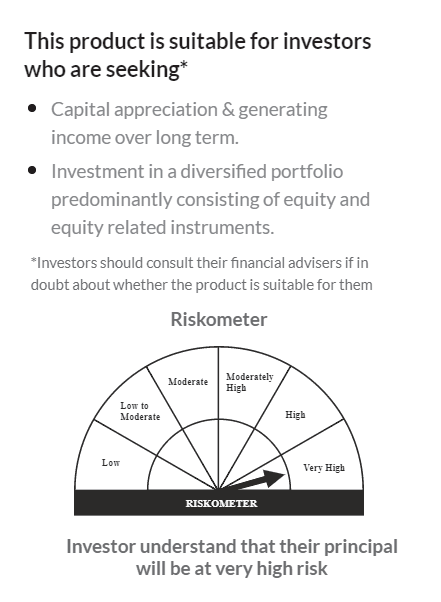

You can consider investing in Axis Long Term Equity Fund. Axis Long Term Equity Fund is an open ended equity linked saving scheme with a statutory lock in of 3 years and tax benefit. The investment objective of Axis Long Term Equity Fund is to generate income and long-term capital appreciation from a diversified portfolio of predominantly equity and equity-related instruments. However, there can be no assurance that the investment objective of the scheme will be achieved.

Decide whether you want to make a lump sum investment or start a monthly SIP

Investors looking to save tax by investing in ELSS fund must decide whether they want to make a one time lump sum investment or opt for a SIP. A lump sum investment is generally made right at the beginning of the investment cycle. On the other hand, if you wish to inculcate some discipline in investing, you can consider starting a SIP. Systematic Investment Plan is an easy and convenient tool to invest in a tax saver fund like ELSS. All an investor has to do is determine their monthly SIP investment amount, decide a date they wish to invest, and complete all the KYC formalities and documentation with the fund house and their bank. Following this, every month on a fixed date, the predetermined amount will be debited from the investor’s savings account and electronically transferred to the fund.

Choose between regular and direct plan

A direct ELSS plan can be brought from the AMC or fund house owning that fund. Because there is no third party involved, the expense ratio of owning a direct plan is low. A regular plan, on the other hand, can be bought though a broker, a mutual fund distributor, or any third party aggregator selling the ELSS scheme. Since there is a third party involved in selling the regular plan, the expense ratio of a regular ELSS plan is generally more than that of the direct plan.

Learn more about investing in ELSS by downloading our Axis ELSS app.

*ELSS Investments are subject to a 3-year lock-in.

#As per the present tax laws, eligible investors (individual/HUF) are entitled to deduction from their gross income of the amount invested in Equity Linked Saving Scheme (ELSS) up to Rs.1.5 lakhs (along with other prescribed investments) under section 80C of the Income Tax Act, 1961. Tax savings of Rs. 46,800 mentioned above is calculated for the highest income tax slab.

Finance Act, 2020 has announced a new tax regime giving taxpayers an option to pay taxes at a concessional rate (new slab rates) from FY 2020-21 onwards. Any individual/ HUF opting to be taxed under the new tax regime from FY 2020-21 onwards will have to give up certain exemptions and deductions. Since, individuals/ HUF opting for the new tax regime are not eligible for Chapter VI-A deductions, the investment in ELSS Funds cannot be claimed as deduction from the total income. Investors are advised to consult his/her own Tax Consultant with respect to the specific amount of tax and other implications arising out of his/her participation in ELSS”

Axis Long Term Equity Fund

An open ended linked saving scheme with a statutory lock in of 3 years and tax benefit

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.

Calculator

View All