ELSS Calculator - Save Tax with the help of ELSS funds

Filing taxes can be tricky, especially with two different options: the old and new tax regimes.

While both offer different rules and deductions, there's an important note for business owners and professionals: if you choose the old regime, that's a one-time, permanent decision (unless you stop having business/professional income).

To simplify things, our income tax calculator is here to help! It's a free and easy tool that estimates your base tax (excluding surcharge & cess) and lets you compare the tax rates of both regimes side-by-side. Want to make smart financial decisions? Learn how our calculator works and see how it can make tax planning a breeze!

- Your Payable Tax

₹0 - Your Tax after investment

₹0 - Amount you save

₹0

Disclaimer: The calculator alone is not sufficient and shouldn't be used for the development or implementation of an investment strategy. This tool is created to explain basic financial / investment related concepts to investors. The tool is created for helping the investor take an informed decision and is not an investment process in itself. Mutual Fund does not provide guaranteed returns. Investors are advised to seek professional advice from financial, tax and legal advisor before investing.

Make small investment for bigger returns

Invest small amount periodically in scheme of your choice

Top Performing Funds to Start your SIP

| Fund Name | AUM(Cr) | Min Investment | This Fund / BenchmarkSI  | Worth of Investment (₹ 10,000)SIP | Expense Ratio | |

|---|---|---|---|---|---|---|

Axis Multicap FundEquity | 10,457.27 | ₹ 100 | 16.09%/13.21% | 8,50,357.13 | 1.11 | |

Axis Nifty Capital Markets Index FundIndex | 99.52 | ₹ 100 | N/A%/N/A% | 29,305.87 | 1.09 | |

Axis NIFTY 100 Index FundIndex | 2,023.81 | ₹ 100 | 12.71%/13.01% | 12,37,374.63 | 0.25 | |

Axis Gold FundFOF - Domestic | 2,827.67 | ₹ 100 | 10.53%/12.01% | 54,15,288.50 | 0.18 | |

Axis Small Cap FundEquity | 29,393.79 | ₹ 100 | 22.64%/18.69% | 61,68,093.50 | 0.77 | |

Axis Value FundEquity | 1,668.17 | ₹ 100 | 16.34%/10.47% | 9,13,670.94 | 0.99 | |

AXIS SILVER FUND OF FUNDFOF - Domestic | 1,148.03 | ₹ 100 | 42.61%/44.36% | 10,96,563.25 | 0.09 | |

Axis Greater China Equity Fund of FundFOF - Overseas | 3,851.80 | ₹ 100 | 3.46%/7.94% | 9,88,125.06 | 0.62 | |

Axis Nifty 500 Index FundIndex | 310.00 | ₹ 100 | 0.44%/0.72% | 2,60,606.36 | 0.16 | |

Axis Nifty Smallcap 50 Index FundIndex | 675.70 | ₹ 100 | 17.22%/18.30% | 8,13,122.75 | 0.34 | |

Invest Now>

Invest Now>

Invest Now>

Invest Now>

Invest Now>

Invest Now>

Invest Now>

AUM as on 30-06-2026 | Expense Ratio as on 03-08-2026

Disclaimer: Returns are calculated on standard investment of Rs 10,000. Click on Scheme Name to know more about Scheme Details.

Past performance may or may not be sustained in future. Please consult your financial advisor before investing. Different plans have different expense structure.

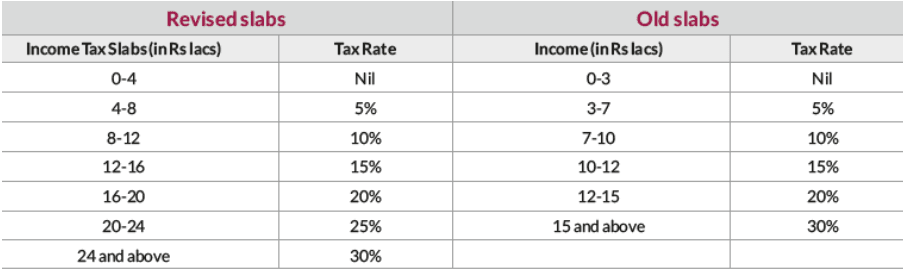

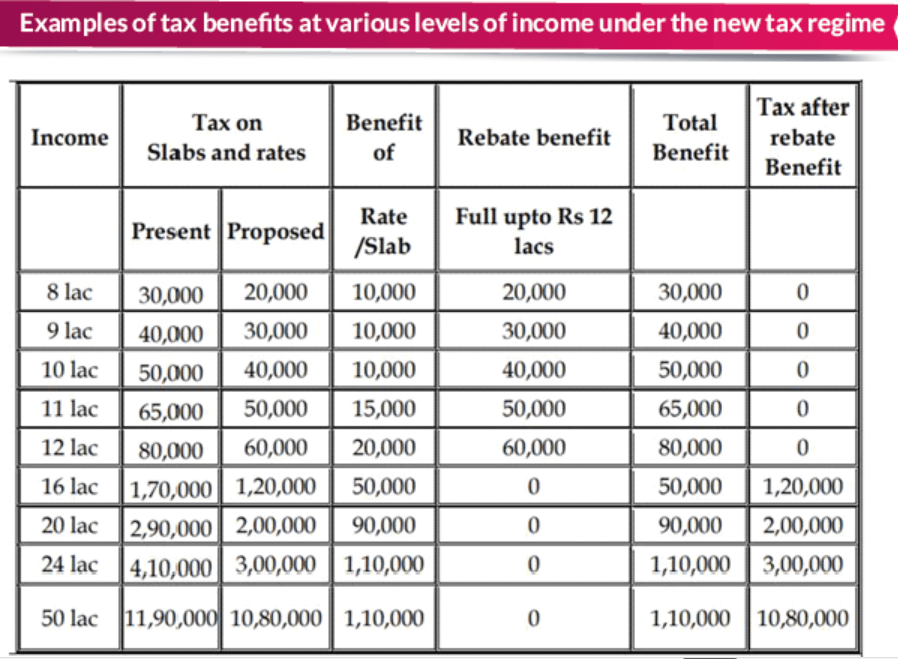

Budget 2025 Update:

- No income tax payable up to normal income (other than special rate income such as Capital Gains) of Rs 12 lakh under the new regime.

- This limit will be Rs 12.75 lakh for salaried taxpayers, due to standard deduction of Rs 75,000

- Roughly 7.5 mn individuals (tax payers) will benefit from the revised slabs.

New Tax Slab vs Old Tax Slab Comparison as per Budget 2025

However, this is a simplified example and doesn't consider income types that are taxed at special rates. Because everyone's tax situation is unique, we recommend consulting with a qualified tax advisor for personalized advice.

Calculators: Your Path to Financial Freedom

SIP Calculator

Want to save for a big goal like a wedding or education? Enter your target amount and timeline to find the monthly SIP needed.

SWP Calculator

Want regular income later? Plan withdrawals to enjoy your savings without worry.

Retirement Calculator

Ready for a stress-free retirement? Estimate the savings you’ll need for your golden years.

Wealth Calculator

Dream of building wealth? See how your investments can grow over the long term.

Lumpsum Calculator

Got a chunk of money to invest? Check how your one-time investment could grow over time.

SIP Top Up Calculator

Boost your SIPs as your income grows. See how small increases can supercharge your savings.

Alpha Calculator

Wondering if your fund beats the market? This tool shows how your fund performs compared to benchmarks.

Sharpe Ratio Calculator

Curious about returns versus risk? Check if your fund gives you bang for your buck.

Sortino Ratio Calculator

Worried about losses? See how your fund handles downside risks for peace of mind.

EMI Calculator

Planning a loan? Find out your monthly EMIs and align them with your investment plans.

CAGR Calculator

Want to compare fund performance? This tool shows the annual growth rate of your investments.

Inflation Calculator

Worried about rising prices? Plan investments to stay ahead of inflation in India.

HRA Calculator

Renting a home? Calculate your HRA tax exemptions to save more money.

STP Calculator

Got a big sum to invest? Plan systematic transfers to spread your money wisely.

Treynor Ratio Calculator

Want to know how your fund fares in volatile markets? This tool measures returns against market swings.

Asset Allocation Calculator

Not sure how to split your money between stocks and bonds? Find the perfect mix for your goals.

SIP Calculator (Monthly SIP Amount Known)

Want to save for a big goal like a wedding or education? Enter your target amount and timeline to find the monthly SIP needed.

Lumpsum Calculator

Got a chunk of money to invest? Check how your one-time investment could grow over time.

SIP Top Up Calculator

Boost your SIPs as your income grows. See how small increases can supercharge your savings.

STP Calculator(I already have an investment)

Got a big sum to invest? Plan systematic transfers to spread your money wisely.

SWP Calculator(I wish to start my SWP immediately)

Want regular income later? Plan withdrawals to enjoy your savings without worry.

Equity Fund Calculator

Love the thrill of stocks? See how equity funds can grow your money.

Debt Fund Calculator

Prefer playing it safe? Check returns from stable debt funds.

Hybrid Fund Calculator

Want growth and safety? Explore returns from funds mixing stocks and bonds.

Balanced Fund Calculator

Like a steady approach? See how balanced funds keep your portfolio stable.

Thematic Fund Calculator

Excited about sectors like tech or green energy? Estimate returns from thematic funds.

Large Cap Fund Calculator

Trust big companies? Calculate returns from stable large-cap funds.

Mid Cap Fund Calculator

Ready for growth with some risk? See how mid-cap funds can boost your wealth.

Small Cap Fund Calculator

Feeling adventurous? Explore returns from small-cap funds.

Multi Cap Fund Calculator

Want a bit of everything? Calculate returns from funds investing across all market sizes.

Index Fund Calculator

Prefer low-cost investing? See how index funds tracking the market perform.FAQs on Income Tax Calculator

Our tool makes it easy to get a rough estimation of your income tax under the new regime. Simply enter your income, and it will generate the tax calculations.

However, this is a simplified example and doesn't consider income types that are taxed at special rates. Because everyone's tax situation is unique, we recommend consulting with a qualified tax advisor for personalized advice.