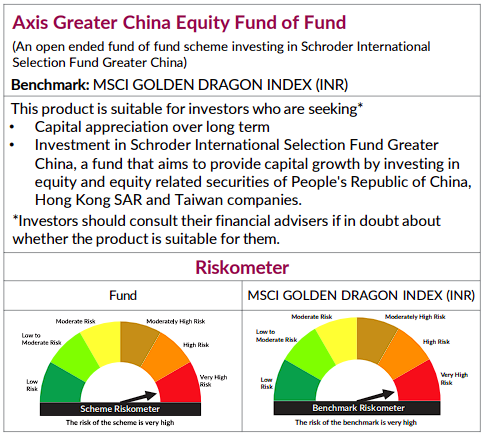

Axis Greater China Equity Fund of Fund: Making Sense of Volatility, Valuations, and the Road Ahead

Markets have tested investor patience over the last few years. Sharp drawdowns, long periods of flat returns, regulatory surprises, and geopolitical noise have led many investors to ask a simple but uncomfortable question:

Is it still worth investing in Greater China?

This article aims to answer that question thoughtfully, using the framework and positioning of Axis Greater China Equity Fund of Fund, which invests in the Schroders ISF Greater China Equity Fund as its underlying strategy.

Rather than reacting to short-term price moves, we’ll focus on structure, risk, recovery potential, and portfolio role.

______________________________________________________________________________

Is this the right time to start or continue an SIP in a Greater China fund?

When markets are volatile and headlines remain uncertain, timing becomes emotionally difficult. This is especially true for China, where recoveries historically tend to be sudden and sharp, often following long stretches of underperformance.

From an investor-behaviour perspective, SIPs are generally more suitable for regions like Greater China. They:

• Smooth entry during volatile phases

• Reduce the pressure of timing a “bottom”

• Allow participation if sentiment turns quickly

The medium-term outlook (12–24 months) for Chinese equities largely depends on policy follow-through, earnings stabilisation, and global liquidity conditions. None of these move in straight lines—but history shows that China cycles tend to turn when pessimism is widespread, not when confidence is high.

________________________________________________________________________________

What about recent negative returns—does recovery still look realistic?

It’s true that Chinese equities have delivered weak returns in 2023–2024, and short-term numbers have been discouraging. However, this phase is not unusual in regional markets driven by policy and confidence cycles.

Recoveries in China have historically been:

• Earnings-led, not narrative-led

• Policy-triggered, not sentiment-driven

• Compressed in time, meaning a large part of returns can occur quickly

Because of this, the recommended holding period for a fund like Axis Greater China Equity Fund of fund is 5 years or more. Investors with shorter horizons may find the volatility uncomfortable.

SIP vs Lumpsum:

• SIP works better when uncertainty is high

• Lumpsum is suitable only if an investor has high conviction and can tolerate drawdowns

• A staggered approach (phased lumpsum) often balances both

_____________________________________________________________________________

What does “Greater China” actually mean in investing terms?

In this fund, “Greater China” includes:

• Mainland China

• Hong Kong

• Taiwan

These markets are deeply interconnected through:

• Trade and supply chains

• Technology and semiconductor ecosystems

• Capital markets and listings

Importantly, allocations are not fixed. Since the underlying Schroders strategy is actively managed, weights across China, Hong Kong, and Taiwan change based on valuations, fundamentals, and opportunity—not index rules.

_______________________________________________________________________________

How does a Fund of Fund structure work here?

Axis Greater China Equity Fund of Fund does not pick stocks directly.

Instead:

• It invests in Schroders ISF Greater China Equity Fund

• Stock selection, sector allocation, and risk management are handled by Schroders

• Axis Mutual Fund provides Indian investors access via a domestic mutual fund structure

Investor returns reflect:

• Performance of the underlying Schroders fund

This structure is designed for access and convenience, not for tactical trading.

_________________________________________________________________________

What does the underlying Schroders strategy actually invest in?

The underlying fund follows a bottom-up stock selection approach, investing across:

• Information Technology*

• Consumer Discretionary

• Communication Services

• Financials

• Industrials

Energy and oil & gas are not structurally large exposures, reflecting the fund’s focus on growth, innovation, and earnings durability rather than commodity cycles.

Portfolio turnover is active but disciplined—there is no fixed rebalance calendar. Positions are reviewed continuously as valuations, earnings, and risks evolve.

___________________________________________________________________________

Do current holdings include AI and semiconductor exposure?

Yes—but selectively.

The portfolio typically includes:

• Semiconductor ecosystem leaders (especially from Taiwan)

• Platform and technology companies aligned with digital and AI adoption

• Industrials and automation beneficiaries

Crucially, the strategy does not chase AI narratives blindly. Exposure is filtered through:

• Cash-flow visibility

• Competitive positioning

• Valuation discipline

This matters in an environment where hype and fundamentals can diverge sharply.

__________________________________________________________________________

How does the fund think about valuations in China today?

Valuations in China are often assessed using a mix of:

• Price-to-Earnings ratio (for consumer and platform businesses)

• Price-to-Book ratio (for financials)

• Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization (for industrials and cyclicals)

Historically, Chinese equities have traded at a discount to developed markets, reflecting higher perceived risk. The key question isn’t whether valuations are “cheap,” but whether earnings and confidence can stabilise.

The underlying strategy focuses on margin sustainability and balance-sheet strength, not just low multiples.

__________________________________________________________________________

What sectors could lead over the next 3–5 years?

While predictions are never certain, areas to watch include:

• Semiconductors and advanced manufacturing (global demand + supply chain positioning)

• Selective consumer recovery plays (linked to income and confidence)

• Industrials and automation (domestic substitution and efficiency)

• Financials and insurance (savings and protection themes)

Earnings growth—not GDP growth—will be the real driver.

__________________________________________________________________________

How do currency movements affect Indian investors?

Returns are influenced by:

• USD/CNY movements (impacting underlying asset values)

• INR/USD movements (impacting returns for Indian investors)

Most overseas FoFs, including this one, do not hedge currency risk systematically. Currency exposure is part of the diversification—but it can amplify volatility in the short term.

___________________________________________________________________________

What are the key risks investors should understand clearly?

This fund carries meaningful risks, including:

• Policy and regulatory uncertainty

• Property-sector stress affecting confidence

• Geopolitical tensions (including China–Taiwan dynamics)

• Export controls and sanctions impacting select sectors

• Periods of high correlation during global risk-off events

The portfolio attempts to mitigate these through diversification, stock selection, and valuation discipline—but risk cannot be eliminated.

__________________________________________________________________________

Does China genuinely diversify an Indian investor’s portfolio?

Over long periods, China has shown imperfect correlation with Indian equities. That said, correlations can rise during global sell-offs.

__________________________________________________________________________

How much allocation makes sense?

As a broad guideline:

• Conservative investors: 0–5%

• Moderate investors: 5–10%

• Aggressive investors: up to 10–15% (only with high risk tolerance)

China-focused exposure should typically be smaller than a diversified global allocation.

__________________________________________________________________________

What about expenses, taxation, and structure considerations?

Fund of Fund structures carry look-through expenses, which are higher than passive ETFs but offer operational simplicity.

Given taxation and volatility, a long holding period is particularly important.

__________________________________________________________________________

So, what is different now—and what should investors realistically expect?

China’s challenge hasn’t been growth, but translation of growth into shareholder returns. What could change outcomes:

• Clearer, sustained policy support

• Earnings normalisation rather than headline optimism

• Valuation discipline and selective positioning

Return expectations should be framed cautiously:

• Short term (12–24 months): volatile, headline-driven

• Long term (3–5 years): outcomes improve if earnings and confidence recover together

__________________________________________________________________________

Final perspective: where does Axis Greater China Equity Fund of Fund fit?

Axis Greater China Equity Fund of Fund is not a tactical trade.

It is a long-term, high-volatility regional allocation, suitable for investors who:

• Understand cyclical and policy-driven markets

• Can stay invested through uncertainty

• Want diversification beyond India and developed markets

Sources: Axis Mutual Fund scheme disclosures and factsheets; Schroders ISF Greater China Equity fund updates and manager commentary; publicly available market research from MSCI, Bloomberg/Reuters, and global macro institutions. Views are for investor education and not investment advice.

Disclaimers:

Sector(s)/ Stock(s)/ Issuer(s) mentioned above are for the purpose of disclosure of the portfolio of the Scheme(s) and should not be construed as recommendation.

Investors will be bearing the recurring expenses of the scheme in addition to the expenses of other schemes in which Fund of Funds scheme makes investment.

The MSCI information may only be used for your internal use, may not be reproduced or disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Axis Bank Ltd. is not liable or responsible for any loss or shortfall resulting from the operation of the scheme.

Past performance may or may not be sustained in future. Please consult your financial advisor before investing.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Are you ready to plan and start your investment journey with Axis?

Download our app

Axis Bank Ltd. is not liable or responsible for any loss or shortfall resulting from the operation of the scheme.

Past performance may or may not be sustained in future. Please consult your financial advisor before investing.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Copyright © 2020. All rights reserved Axis Mutual Fund.

Connect with us :![]()

![]()

![]()

![]()

![]()

![]()

Privacy | Terms of Use | Disclaimer | Sitemap