Manufacturing gains momentum in India’s broad-based expansion

Since 2025, India’s macro and equity markets have been shaped less by domestic tailwinds and more by persistent global headwinds. The economy has navigated sustained FII outflows, phases of muted or negative equity returns, rising protectionism through trade and tariff frictions and geopolitical tensions in West Asia that have disrupted energy markets and supply chains. These pressures are particularly relevant for India, given its dependence on imports for over 85% of its energy needs, making it highly sensitive to global commodity shocks.

Typically, such an environment leads to uneven growth, with only a few sectors performing while the broader economy slows. India’s experience has been different. Recent data shows that growth has held up moderately well and more importantly, it has been broad-based. Consumption remains stable, services are strong and manufacturing is now gaining traction – pointing to a multi-engine expansion rather than sector specific recovery.

A shift towards more balanced growth

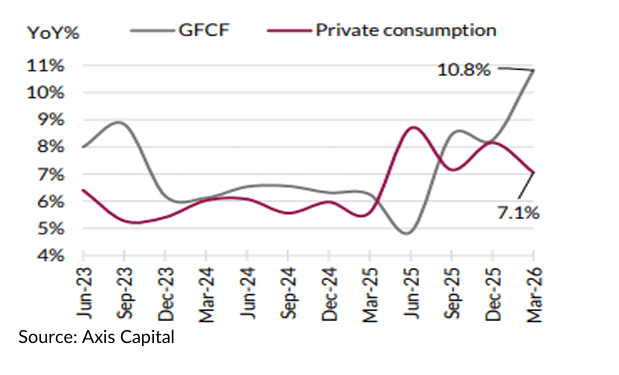

India ended FY26 with real GDP growth of 7.7%, supported by a strong 7.8% expansion in Q4FY26. Beneath this headline lies a more important shift - the composition of growth is becoming increasingly balanced.

While consumption continues to provide a stable foundation, investment activity has strengthened meaningfully, with gross fixed capital formation expanding 10.8% in Q4FY26 and emerging as the largest contributor on the demand side.

This marks an important evolution. India’s growth has historically been consumption driven. The current phase is different - investment is now supporting consumption, creating a more durable cycle - where capex not only drives near-term growth but also builds future capacity - particularly relevant for manufacturing..

Corporate data validates the macro story

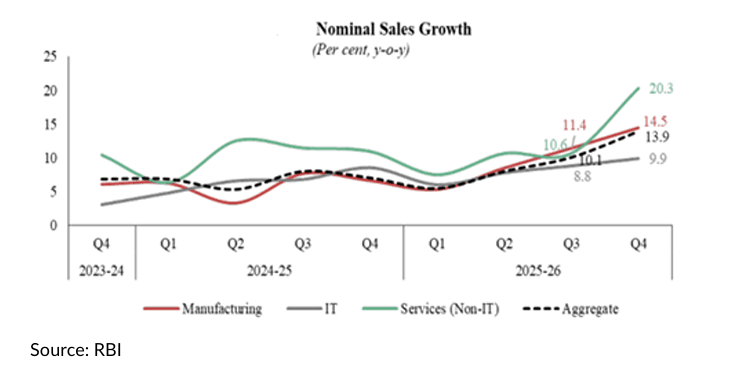

Bottom-up indicators reinforce this improving macro picture. The Reserve Bank of India’s (RBI) corporate data shows aggregate sales growth of 13.9% YoY in Q4FY26 across 3,266 listed companies, with clear acceleration across sectors. Manufacturing sales grew 14.5%, up from 11.4% in the prior quarter, services growth remained strong, with non-IT services expanding at over 20% and IT services also showed steady improvement.

Importantly, this alignment between GDP data and corporate performance suggests that growth is not just statistical, but visible across industries and supported by underlying demand.

Services and Financials provide stability

Services continue to anchor growth, led by strong domestic demand and improving business activity. Within this, financials play a critical enabling role. Strengthened balance sheets, improved asset quality and higher capital buffers, supported by years of balance sheet clean up, have positioned banks to support incremental credit growth across retail, MSMEs and corporate capex.

As a result, banks are not just beneficiaries of growth but key drivers ensuring the smooth flow of credit across the economy and supporting both consumption and the investment cycle.

Manufacturing: strengthening within a broad-based expansion

Within India's broad-based expansion, manufacturing is emerging as an increasingly important growth driver. Its significance lies not in replacing consumption or services, but in adding another engine to growth, making the expansion more balanced and resilient.

Recent data points to a clear improvement in momentum. RBI data shows manufacturing sales growth accelerated to 14.5% in Q4FY26 from 11.4% in the previous quarter, supported by strong demand across automobiles, electrical machinery and metals. Healthy consumer demand continues to support segments such as passenger vehicles and two-wheelers, while rising public and private capex is driving demand for capital goods, industrial machinery and construction-related inputs.

Corporate earnings trends reinforce this picture. Automobile companies reported robust revenue and earnings growth, while capital goods companies continue to benefit from strong order inflows across power transmission, defence, renewables and data-centre infrastructure. Together, these trends indicate that the manufacturing recovery is becoming increasingly broad-based.

Beyond output and earnings, manufacturing is also contributing to a gradual improvement in the quality of growth. According to the Periodic Labour Force Survey 2025 by Ministry of Statistics & Programme Implementation (MOSPI), manufacturing's share of total employment increased to 12.1% in 2025 from 11.6% in 2024, highlighting the sector's growing role in employment generation and ongoing labour-market transformation.

As manufacturing scales up, it creates demand across suppliers, MSMEs, logistics providers and service industries, generating multiplier effects that support wider economic activity. Greater scale and efficiency are also improving export competitiveness, enabling Indian companies to participate more actively in global supply chains.

Resilience amid cost pressures

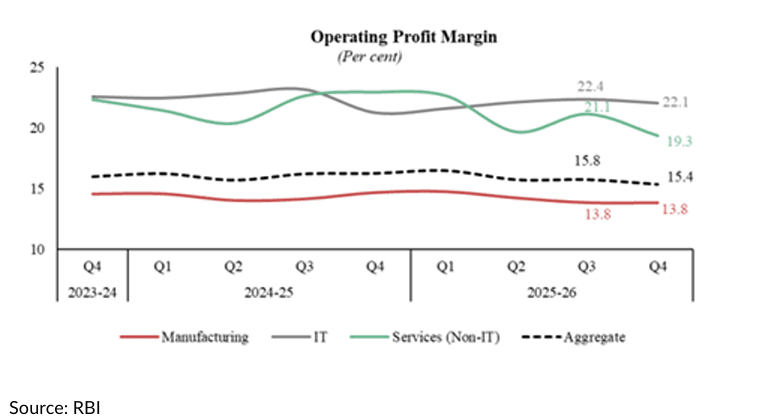

A defining feature of the current cycle is manufacturing’s resilience to elevated input costs driven by commodity volatility, energy prices and supply chain disruptions.

Despite these pressures, margins have remained broadly stable and financial performance has continued to improve. This reflects a clear shift in corporate behaviour marked by stronger pricing discipline, tighter cost controls, improved operational efficiency and healthier balance sheets.

Underlying this resilience is the significant deleveraging undertaken over recent years. Improved interest coverage ratios and stronger balance sheets have enhanced the sector’s ability to absorb shocks. Unlike earlier cycles, where cost pressures often resulted in margin compression and curtailed investment, companies today are better positioned to sustain capex even in volatile conditions. It not only supports near-term growth but also strengthens the foundations for a more durable industrial expansion.

Earnings are reflecting this shift

The shift is now clearly visible in earnings. Growth is no longer concentrated in a few sectors but is broadening across the corporate landscape. In Q4FY26, aggregate earnings of the Nifty 500 grew 16% YoY in Q4FY26, while earnings excluding financials rose 17% YoY. Even after excluding commodities such as metals and oil & gas, earnings growth remained a healthy 12% YoY, highlighting the breadth of the recovery. Notably, sales growth of 12% YoY was the strongest seen in the past 13 quarters, reflecting improving demand across the economy.

The strength has been particularly visible across manufacturing and investment-linked sectors. Automobiles delivered 23% YoY earnings growth, infrastructure companies reported 15% growth, capital goods companies recorded 8% growth, while real estate and retail companies posted 20% and 45% growth respectively. Midcap companies have emerged as a major engine of this earnings expansion, with aggregate profits of the Nifty Midcap 150 rising 34% YoY, significantly ahead of large caps and small caps.

Earnings participation has broadened meaningfully at the company level, with around half of the Nifty 500 delivering earnings growth of over 15% YoY during the quarter, and 14 of 23 major sectors reporting double-digit profit growth. This wider dispersion reduces reliance on a narrow set of sectors and reflects a more balanced and resilient earnings cycle.

Near term moderation, long term strength

Growth is expected to moderate in FY27 from the strong pace seen in FY26, reflecting base effects and an uncertain global environment. However, this moderation should be viewed as a normalization rather than a reversal. The underlying drivers of growth remain intact, with consumption, services, investment and manufacturing all contributing to economic activity, creating a more balanced and resilient expansion.

Recent easing of geopolitical tensions in West Asia has also reduced concerns around prolonged disruptions to global energy supplies. For India, a more stable energy environment can help contain inflation, improve corporate costs and support manufacturing oriented sectors such as automobiles, industrials, specialty chemicals and capital goods. Combined with healthy corporate balance sheets, continued infrastructure spending and strengthening domestic capex, this provides a constructive backdrop for the manufacturing cycle.

Positioning for a manufacturing led expansionAgainst this backdrop, portfolio positioning remains aligned with a broadening and increasingly structural growth cycle. Financials continue to form the core, given their central role in funding both consumption and capex. At the same time, opportunities are expanding across manufacturing and industrial ecosystems. We see opportunities arising from policy support, supply-chain diversification, infrastructure investments and India's increasing focus on building domestic manufacturing capabilities.

Accordingly, we remain overweight on sectors directly linked to India’s manufacturing and industrial ecosystem. Automobiles and auto ancillaries, electronics manufacturing services (EMS), defence, capital goods, pharmaceuticals and contract development and manufacturing organizations (CDMOs), and specialty chemicals are central to this positioning. These sectors are benefiting from a combination of domestic demand growth, infrastructure spending, production-linked incentives and emerging themes such as energy transition, digitization and data centre build-outs. Many of these industries are also becoming increasingly integrated into global supply chains, with export-oriented segments such as specialty chemicals and electronics manufacturing well positioned to gain from the ongoing diversification of global sourcing towards India.

A structural theme underpinning this view is India’s increasing focus on self-reliance—across manufacturing, defence, electronics and energy. Investments in renewable energy, transmission, and domestic production capabilities are not only reducing import dependence but also building globally competitive ecosystems.

Overall, our positioning is aligned with a manufacturing cycle that is becoming increasingly structural and broad-based—driven not just by cyclical recovery but by sustained investment, improving competitiveness and stronger corporate balance sheets. The focus remains on companies that can capture incremental demand, adapt to evolving supply chains and maintain margins through cost pressures, positioning portfolios to benefit from a more durable manufacturing-led growth cycle.

Source: Axis Capital, RBI, Axis MF Research, Motilal Oswal, MOSPI

Disclaimer: This document represents the views of Axis Asset Management Co. Ltd. and must not be taken as the basis for an investment decision. Neither Axis Mutual Fund, Axis Mutual Fund Trustee Limited nor Axis Asset Management Company Limited, its Directors or associates shall be liable for any damages including lost revenue or lost profits that may arise from the use of the information contained herein. No representation or warranty is made as to the accuracy, completeness or fairness of the information and opinions contained herein. The AMC reserves the right to make modifications and alterations to this statement as may be required from time to time.

The sectors mentioned herein are for general assessment purpose only and not a complete disclosure of every material fact. It should not be construed as investment advice to any party. The schemes may or may not have any investments in stocks under these sectors.

Investors are requested to consult their financial, tax and other advisors before taking any investment decision(s).

Axis Bank Limited is not liable or responsible for any loss or shortfall resulting from the operation of the scheme.

Mutual Fund Investments are subject to market risks, read all scheme related documents carefully.Calculator

View All