► Markets do remain overvalued across the investment part of the economy and we may see

normalisation in some of these segments.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one’s risk appetite and future goals in life.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one’s risk appetite and future goals in life.

► Expect a pause post the December rate cut.

► Yield upside limited; investors should add short term bonds with every rise in yields.

► Short term 2-5-year corporate bonds, tactical mix of long duration Gsecs and income plus arbitrage are best strategies to invest in the current macro environment.

► Selective Credits continue to remain attractive from a risk reward perspective given the improving macro fundamentals.

► Yield upside limited; investors should add short term bonds with every rise in yields.

► Short term 2-5-year corporate bonds, tactical mix of long duration Gsecs and income plus arbitrage are best strategies to invest in the current macro environment.

► Selective Credits continue to remain attractive from a risk reward perspective given the improving macro fundamentals.

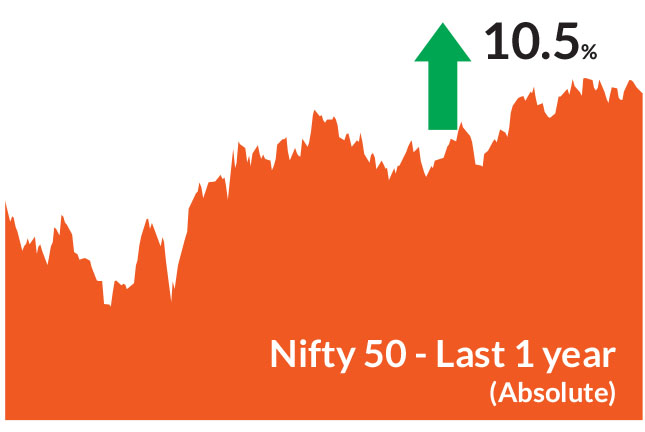

After three consecutive months of positive returns, equities ended the

month lower. For most part of the month, equities remained rangebound

impacted by concerns over the India-US trade deal. Large caps

outperformed mid and small caps. The BSE Sensex and Nifty 50 closed 0.6%

and 0.3% down, while the NSE Midcap 100 fell by 0.9% and the NSE

Smallcap 100 by 0.6%. On the sectoral front, metals, oil & gas and auto were

the top gainers, whereas capital goods, consumer durables and realty were

the top losers. Foreign Portfolio Investors (FPIs) sold equities to the tune of

US$2.5bn while Domestic Institutional Investors (DIIs) remained

supportive with US$8.1bn in equity purchases. Year to date, FPI outflows

total US$19bn while the DIIs bought to the tune of US$89.5bn.

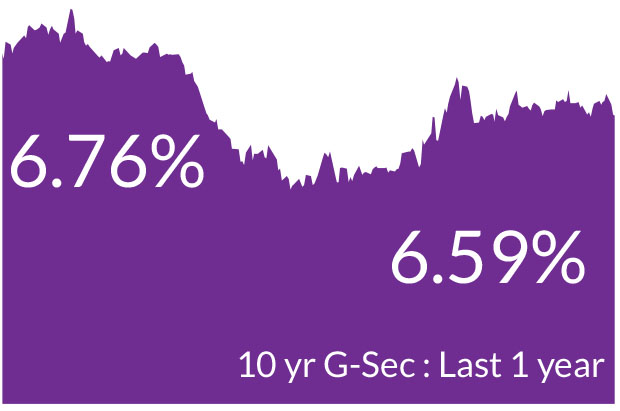

Bond yields traded higher over the month with the 10-year benchmark government bond yield rising 10 basis points to end at 6.59%. US Treasury yields also rose, with the 10-year yield ending the month at 4.17%.

Banking liquidity in positive : On December 23, the RBI announced a series of measures to inject durable liquidity into the banking system amid FX interventions and rising yields. Key actions include: 1) OMO Purchases of Rs 2trn in four tranches of Rs 500 billion each, scheduled for a) December 29, 2025 b) January 05, 2026 c) January 12, 2026 and 4) January 22, 2026. In addition, a US$10 billion, 3-year buy/sell swap has been slated for January 13, 2026.

Earlier, in its December policy meeting, the RBI had initiated liquidity infusion through OMO purchase auctions of Government of India securities worth Rs 1 lac cr, conducted in two tranches of Rs 50,000 cr each on December 11, 2025, and December 18, 2025 and a USD/INR Buy/Sell Swap auction of US$ 5 billion for a tenor of three years held on December 16, 2025.

Inflation rebounds from lows : CPI inflation rose to 0.71% in November from a record low of 0.25% in October. Inflation remains quite low due to a) weak food inflation, concentrated in vegetables, pulses and spices b) weaker core goods inflation as GST cuts are passed through. The central bank in its December monetary policy revised inflation forecasts upwards and expects inflation to stand at 0.6% in December and rise to 2% for FY26.

Bond yields traded higher over the month with the 10-year benchmark government bond yield rising 10 basis points to end at 6.59%. US Treasury yields also rose, with the 10-year yield ending the month at 4.17%.

Key Market Events

RBI lowers rates in December policy : the Monetary Policy Committee (MPC) of the RBI lowered interest rates by 25 bps to 5.25% and maintained a neutral stance. This decision was shaped by a "goldilocks" backdrop-robust growth and exceptionally low inflation despite a weaker currency.Banking liquidity in positive : On December 23, the RBI announced a series of measures to inject durable liquidity into the banking system amid FX interventions and rising yields. Key actions include: 1) OMO Purchases of Rs 2trn in four tranches of Rs 500 billion each, scheduled for a) December 29, 2025 b) January 05, 2026 c) January 12, 2026 and 4) January 22, 2026. In addition, a US$10 billion, 3-year buy/sell swap has been slated for January 13, 2026.

Earlier, in its December policy meeting, the RBI had initiated liquidity infusion through OMO purchase auctions of Government of India securities worth Rs 1 lac cr, conducted in two tranches of Rs 50,000 cr each on December 11, 2025, and December 18, 2025 and a USD/INR Buy/Sell Swap auction of US$ 5 billion for a tenor of three years held on December 16, 2025.

Inflation rebounds from lows : CPI inflation rose to 0.71% in November from a record low of 0.25% in October. Inflation remains quite low due to a) weak food inflation, concentrated in vegetables, pulses and spices b) weaker core goods inflation as GST cuts are passed through. The central bank in its December monetary policy revised inflation forecasts upwards and expects inflation to stand at 0.6% in December and rise to 2% for FY26.

Equity Market View:

The Reserve Bank of India’s accommodative stance, characterized by proactive rate cuts and ample liquidity, has created a supportive backdrop for growth. Coupled with fiscal measures like GST rationalization, tax cuts, MSME support, and regulatory reforms by RBI and SEBI, these initiatives have laid a strong foundation for India’s structural recovery. India’s macroeconomic stability will be underpinned by fiscal consolidation efforts, benign oil prices, and steady global growth. Domestic consumption demand is expected to remain buoyant, driven by premiumization trends, rural recovery supported by agricultural activity, and fiscal support from state governments. These factors collectively create a favorable backdrop for sustained economic expansion. The resolution of tariff issues between the US and India can help accelerate recovery.Earnings have likely bottomed in India and we could see a broad-based recovery in CY26. Markets expect mid teen EPS growth 2026, with reduced risks of downgrades compared to 2025. Over the 18 months, earnings estimates in India were lowered. However, the picture is looking better over the last three months with positive developments, such as GST rate cuts (key beneficiaries being autos, followed by consumer staples). High frequency indicators are reflecting improvements. Financials, IT services and auto estimates have been stable in the last three months, while construction materials, realty and metals have seen upgrades.

The market is expected to continue its focus on high earnings visibility, sustained profitability and structural growth catalysts along with reasonable valuations. While bottom-up stock picks around popular themes remain expensive, underperformers due to slower growth with relatively attractive valuations offer selective opportunities. Stock picking with a focus on growth at reasonable valuations will remain the cornerstone of performance, with a clear preference for domestic-oriented sectors over export-heavy plays.

Overall, we maintain an overweight stance on consumption. The positive impact of GST rationalization is seen across consumer discretionary companies who have reported strong festive-season sales. We also remain constructive on other consumer discretionary plays—especially in retail, hospitality, and travel & tourism—which are gaining from strengthening domestic momentum. In automobiles, the trend toward premiumization is expected to strengthen, supported by a pickup in the replacement cycle. Recent consumption numbers and management commentaries suggest that consumption sector has gained post GST rationalization however continuity in revival needs to be seen in coming months.

Fixed Income Market view

Globally, disinflation has largely run its course and inflation seems close to its trough. While inflation trends across major economies could diverge in 2026, the key driver globally remains rising commodity prices. Any sustained increase in these prices could set the tone for inflation going forward. In 2025, commodities such as gold, silver and industrial metals saw notable gains, even as brent crude stayed subdued. In the US, inflation pressures are likely to remain sticky, fueled by tight labor markets, elevated wages, and persistent service-sector costs amid lingering supply constraints.Despite concerns that reciprocal tariffs would dampen growth, the US economy has remained strong. According to the latest IMF projections, US GDP is expected to expand by 2.1% in 2026, while Europe is forecast to grow at a healthy 1.7%. China is likely to maintain strong momentum with 5% growth and India is projected to lead with 6.2%. Against this backdrop, monetary easing may stay limited. The Fed is expected to cut rates by an additional 50 basis points in 2026, while the BoJ could raise rates by 25 basis points. Meanwhile, the European Central Bank is anticipated to hold steady, ensuring policy stability across the Eurozone.

Since February 2025, we have been steadily reducing portfolio duration, shifting away from long-duration strategies toward accrual-focused approaches. This year, we see accrual and selective tactical duration as the dominant themes, particularly in long bonds and state development loans (SDLs).

In this context, a barbell strategy emerges as the most effective approach—balancing short-tenor bonds for liquidity with long-duration bonds for tactical opportunities. Our preferred positioning includes 2-year AA-rated corporate bonds for steady accrual and long-tenor government securities for duration plays, offering a combination of consistent accrual and potential upside.

Source: Bloomberg, Axis MF Research.