► Markets do remain overvalued across the investment part of the economy and we may see

normalisation in some of these segments.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► Rate cycle on a pause for the next few policies.

► Yield upside limited; investors should add short term bonds with every rise in yields.

► Short term 2-5-year corporate bonds and tactical mix of 8-10 yr Gsecs and are best strategies to invest in the current macro environment.

► Selective Credits continue to remain attractive from a risk reward perspective given the improving macro fundamentals.

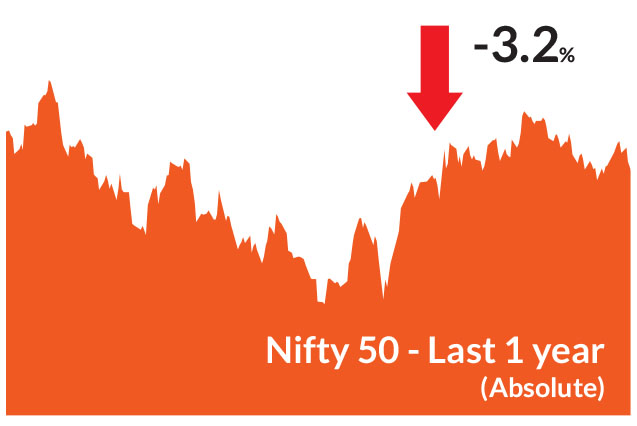

Indian equities continued to remain impacted by the evolving tariff scenario

particularly with the additional 25% tariffs kicking in. The BSE Sensex and

Nifty 50 ended the month with declines of 1.7% and 1.4%, respectively. The

mid and small-cap indices underperformed, with the NSE Midcap 100

declining by 2.9% and NSE Smallcap 100 falling by 4.1%, reflecting

heightened caution among investors. Consumption-oriented sectors saw a

rally on the government's plan for rationalization of GST. Auto and

consumer durables sectors were up 5.8% and 2%, respectively. Oil & gas,

power and realty were down 4.7%,4.6% and 4.5%, respectively. Globally, US

equities remained buoyant, continuing with their gains for the fourth

consecutive month; the S&P 500 touched lifetime highs, supported by

continued strength from mega cap stocks.

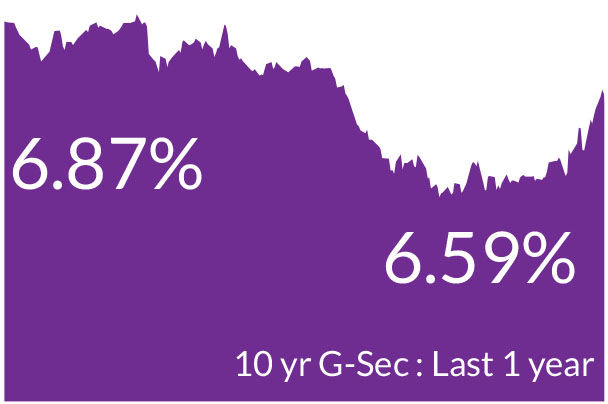

Bond yields saw a notable rise over the month, leading to a steepening of the yield curve. The 10-year benchmark government bond yield climbed 22 basis points to end at 6.62%, as investor sentiment was weighed down by the implementation of higher tariffs and the absence of any resolution on that front. In contrast, US Treasury yields edged lower, with the 10-year yield ending the month at 4.23%, driven by growing expectations of a potential rate cut by the US Federal Reserve (Fed).

Key highlights of the Proposed GST Overhaul are 1) Simplified Structure: Transition from the current four-tier GST system (5%, 12%, 18%, 28%) to a streamlined two-slab structure - 5% merit rate and 18% standard rate. 2) Special Rate for Sin & Luxury Goods: A 40% special rate proposed for items such as tobacco, alcohol, and high-end luxury products. 3) Lower Tax on Essentials: Most daily-use items to be taxed at 5%, making them more affordable for consumers. 4) Reclassification of High-Tax Items: Approximately 90% of items currently under the 28% slab will be moved down to the 18% slab. 5) Reduction in Mid-Tier Tax Items: Around 99% of items from the 12% slab will shift to the lower 5% slab. 6) Exclusions: Petroleum products will remain outside the GST framework.

Q1FY26 earnings: Nifty 50 EPS grew 7% in Q1FY26, the proportion of misses in small caps was the largest, followed by large caps and midcaps; 43% of smallcap companies missed expectations, while the misses were relatively lower in midcaps and large caps at 28% and 29% respectively. The quarter saw earnings downgrades for FY26/27, indicating rising global uncertainty, with Auto ancillaries, Capital Goods, Pharma and IT witnessing the highest downgrades. Alongside weak earnings, tariff uncertainty-given the absence of an extension on the additional 25% duty deadline for India-continues to weigh on sentiment.

Valuations: Valuations remain expensive on an absolute basis and trading well above long-term averages. The challenge faced by domestic fund managers is that they are receiving substantial monthly inflows, hitting record highs of late, while they are faced with deploying the cash into a relatively thin equity market. India's equity risk premium has risen significantly above its ten-year average, suggesting that current index levels may not fully reflect the strength of underlying fundamentals. This divergence indicates that investors could be undervaluing the long-term growth potential and macro stability embedded in the economy, despite elevated market valuations.

Inflation falls further : Headline inflation further fell to 1.55% in July from 2.1% in June, led by a faster than expected moderation in food prices especially vegetables. Overall food CPI could record mild positive growth in August after remaining in deflation for two months in a row, while core CPI remains largely range-bound. As the favourable base effect dissipates, we expect headline CPI to inch up. The IMD's forecast of an above-normal monsoon is likely to support the crop harvests, which, in addition to the healthy buffer stocks, is likely to ensure that food prices remain benign. Crude oil prices fell 6.1% over the month amid reduced demand and increased oil supply.

GDP data comes in stronger : India's real GDP growth surged to 7.8% in Q1FY26 (up from 7.4% in Q4FY25, largely due to a significantly lower GDP deflator of 0.9% compared to 3.1% in the previous quarter. This came on the back of nominal GDP growth slowing to 8.8% from 10.8%. The growth was broad-based, with gross fixed capital formation (GFCF) rising 7.8%, private consumption growing 7.0%, and government consumption rebounding sharply by 7.4%, aided by a low base in Q1FY25 due to election-related spending slowdown. The tariff related headwinds could be offset by GST rationalization.

Rupee depreciates in July : While the US Dollar remained largely rangebound through August-with the DXY slipping just 0.2%, the Rupee came under pressure, depreciating by 0.7% against the dollar. This made our currency one of the weakest performers in the region. The depreciation was primarily driven by lingering uncertainty around tariffs, which weighed on investor sentiment.

US treasury yields fall : The yields on US Treasuries fell towards the end of the month after the Fed chair signaled that interest rate cuts could be on the horizon in light of deteriorating financial conditions. He also said that the central bank was moving "carefully" when it comes to monetary policy.

Banking liquidity remains in surplus : Banking liquidity surplus improved more than anticipated, primarily driven by robust month-end government spending. Looking ahead, we expect liquidity surplus to strengthen further, supported by continued government expenditure. Additionally, the upcoming CRR rate cuts will provide further relief, helping to counterbalance the seasonal rise in currency in circulation. These factors collectively point to a more accommodative liquidity environment in the near term.

Bond yields saw a notable rise over the month, leading to a steepening of the yield curve. The 10-year benchmark government bond yield climbed 22 basis points to end at 6.62%, as investor sentiment was weighed down by the implementation of higher tariffs and the absence of any resolution on that front. In contrast, US Treasury yields edged lower, with the 10-year yield ending the month at 4.23%, driven by growing expectations of a potential rate cut by the US Federal Reserve (Fed).

Key Market Events

GST rationalization: During the month, the government announced a major overhaul of the GST framework, introducing a simplified two-slab system aimed at making essential goods more affordable, reducing tax-related disputes, and boosting domestic consumption. Notably, this reform follows the Rs 1 trillion in income tax incentives unveiled in Budget 2025-marking a direct policy push to accelerate India's consumption-driven growth cycle. The key test is whether this fiscal push, reinforced by monetary easing and a good monsoon, can finally unlock India's muted consumption cycle. The proposed GST reforms are expected to significantly benefit sectors such as consumer durables, automobiles (including two-wheelers, small cars, tractors, and commercial vehicles), cement, staples/FMCG, and retail. As most of these categories move into lower tax slabs, improved affordability is likely to drive higher consumption and support volume growth.Key highlights of the Proposed GST Overhaul are 1) Simplified Structure: Transition from the current four-tier GST system (5%, 12%, 18%, 28%) to a streamlined two-slab structure - 5% merit rate and 18% standard rate. 2) Special Rate for Sin & Luxury Goods: A 40% special rate proposed for items such as tobacco, alcohol, and high-end luxury products. 3) Lower Tax on Essentials: Most daily-use items to be taxed at 5%, making them more affordable for consumers. 4) Reclassification of High-Tax Items: Approximately 90% of items currently under the 28% slab will be moved down to the 18% slab. 5) Reduction in Mid-Tier Tax Items: Around 99% of items from the 12% slab will shift to the lower 5% slab. 6) Exclusions: Petroleum products will remain outside the GST framework.

Q1FY26 earnings: Nifty 50 EPS grew 7% in Q1FY26, the proportion of misses in small caps was the largest, followed by large caps and midcaps; 43% of smallcap companies missed expectations, while the misses were relatively lower in midcaps and large caps at 28% and 29% respectively. The quarter saw earnings downgrades for FY26/27, indicating rising global uncertainty, with Auto ancillaries, Capital Goods, Pharma and IT witnessing the highest downgrades. Alongside weak earnings, tariff uncertainty-given the absence of an extension on the additional 25% duty deadline for India-continues to weigh on sentiment.

Valuations: Valuations remain expensive on an absolute basis and trading well above long-term averages. The challenge faced by domestic fund managers is that they are receiving substantial monthly inflows, hitting record highs of late, while they are faced with deploying the cash into a relatively thin equity market. India's equity risk premium has risen significantly above its ten-year average, suggesting that current index levels may not fully reflect the strength of underlying fundamentals. This divergence indicates that investors could be undervaluing the long-term growth potential and macro stability embedded in the economy, despite elevated market valuations.

Inflation falls further : Headline inflation further fell to 1.55% in July from 2.1% in June, led by a faster than expected moderation in food prices especially vegetables. Overall food CPI could record mild positive growth in August after remaining in deflation for two months in a row, while core CPI remains largely range-bound. As the favourable base effect dissipates, we expect headline CPI to inch up. The IMD's forecast of an above-normal monsoon is likely to support the crop harvests, which, in addition to the healthy buffer stocks, is likely to ensure that food prices remain benign. Crude oil prices fell 6.1% over the month amid reduced demand and increased oil supply.

GDP data comes in stronger : India's real GDP growth surged to 7.8% in Q1FY26 (up from 7.4% in Q4FY25, largely due to a significantly lower GDP deflator of 0.9% compared to 3.1% in the previous quarter. This came on the back of nominal GDP growth slowing to 8.8% from 10.8%. The growth was broad-based, with gross fixed capital formation (GFCF) rising 7.8%, private consumption growing 7.0%, and government consumption rebounding sharply by 7.4%, aided by a low base in Q1FY25 due to election-related spending slowdown. The tariff related headwinds could be offset by GST rationalization.

Rupee depreciates in July : While the US Dollar remained largely rangebound through August-with the DXY slipping just 0.2%, the Rupee came under pressure, depreciating by 0.7% against the dollar. This made our currency one of the weakest performers in the region. The depreciation was primarily driven by lingering uncertainty around tariffs, which weighed on investor sentiment.

US treasury yields fall : The yields on US Treasuries fell towards the end of the month after the Fed chair signaled that interest rate cuts could be on the horizon in light of deteriorating financial conditions. He also said that the central bank was moving "carefully" when it comes to monetary policy.

Banking liquidity remains in surplus : Banking liquidity surplus improved more than anticipated, primarily driven by robust month-end government spending. Looking ahead, we expect liquidity surplus to strengthen further, supported by continued government expenditure. Additionally, the upcoming CRR rate cuts will provide further relief, helping to counterbalance the seasonal rise in currency in circulation. These factors collectively point to a more accommodative liquidity environment in the near term.

Equity Market View:

The current earnings momentum, combined with supportive policy measures, has laid the groundwork for a potential revival in the second half of FY26. Key enablers include easing interest rates, anticipated income-tax relief, GST rationalization, post-election fiscal initiatives, improved liquidity conditions, and a likely rebound in rural demand following a favorable monsoon-all of which could collectively boost consumption and economic activity.Against the backdrop of lower interest rates, expected GST rationalisation, and a likely boost in consumption, we continue to maintain an overweight stance on the consumption theme. If these macro tailwinds are effectively passed on to end consumers, they could reset India's consumption cycle. For instance, benefits in sectors like cement and building materials could enhance housing affordability, which in turn may stimulate the credit cycle. This underpins our overweight position in the financial sector, particularly NBFCs, which are well-positioned to benefit from increased credit demand and improved liquidity conditions.

We also remain constructive on consumer discretionary plays-especially in retail, hospitality, and travel & tourism-which are poised to gain from strengthening domestic momentum and festive season demand. Our GDP numbers validate our stance. While we've trimmed our overweight in automobiles, we retain an overweight in pharmaceuticals despite some pricing headwinds in the US. We remain underweight in IT. Additionally, we are positive on structural themes such as renewable capex, power transmission, and defense, where we've recently increased exposure. Overall, India continues to offer a compelling medium- to long-term growth opportunity, supported by resilient domestic demand, a favorable rural outlook post-monsoon, and supportive macroeconomic indicators.

Debt Market View:

There were quite a few variables at play in the domestic markets, nervousness about tariffs, the S&P upgraded, GST rationalization and strong GDP growth. The rating upgrade by S&P has been backed by buoyant economic growth, commitment to fiscal consolidation, improved quality of spending (capex at 3.1% of GDP), anchored inflation expectations amid policy continuity. However, while this improves the investment climate for India, a rating upgrade does not necessarily impact bond markets to quite an extent.In our Acumen - "Unlocking tactical opportunities in a dislocated bond market", we have highlighted that the recent sell-off has caused a dislocation in the bond market, where short-term bonds have outperformed long-term ones. However, this has also created tactical opportunities for informed investors. The sell-off has pushed bond yields, particularly for government bonds, back to levels seen before the recent rate-cut cycle began. This offers a more attractive entry point for investors. There's a possibility of a 15-25 bps rally in long duration bonds in the near term. This could be triggered by several factors, including:

• Growth headwinds: Any additional tariffs or economic developments that weaken India's growth outlook could prompt the RBI to deploy additional policy tools, such as a rate cut, to stimulate the economy.

• Global Shifts in Monetary policy: A dovish stance by the US Federal Reserve driven by unemployment concerns could lead to rate cuts, thus supporting global and Indian bond yields.

• RBI Intervention: To stabilize yields and mitigate market volatility, the RBI may consider conducting targeted Open Market Operations (OMOs) in limited quantities. Additionally, in response to prevailing demand-supply mismatches, the central bank could recalibrate the upcoming auction calendar for October 2025 to March 2026 by reducing the proportion of long-duration bond issuances within the overall borrowing program.

Meanwhile, in the US, the Fed has indicated a rate cut on the horizon and this supports our view of two rate cuts in 2025. Indicators such as a softening labor market and tariff-related growth headwinds support this view. The cumulative easing could total 75-100 basis points, especially if trade tensions persist and fiscal policy remains tight.

Source: Bloomberg, Axis MF Research.